Middle East Escalation Disrupts Global Ocean and Air Freight Networks

- The Port of Salalah has suspended operations until further notice, following a drone attack yesterday that hit several of the port’s fuel storage tanks.

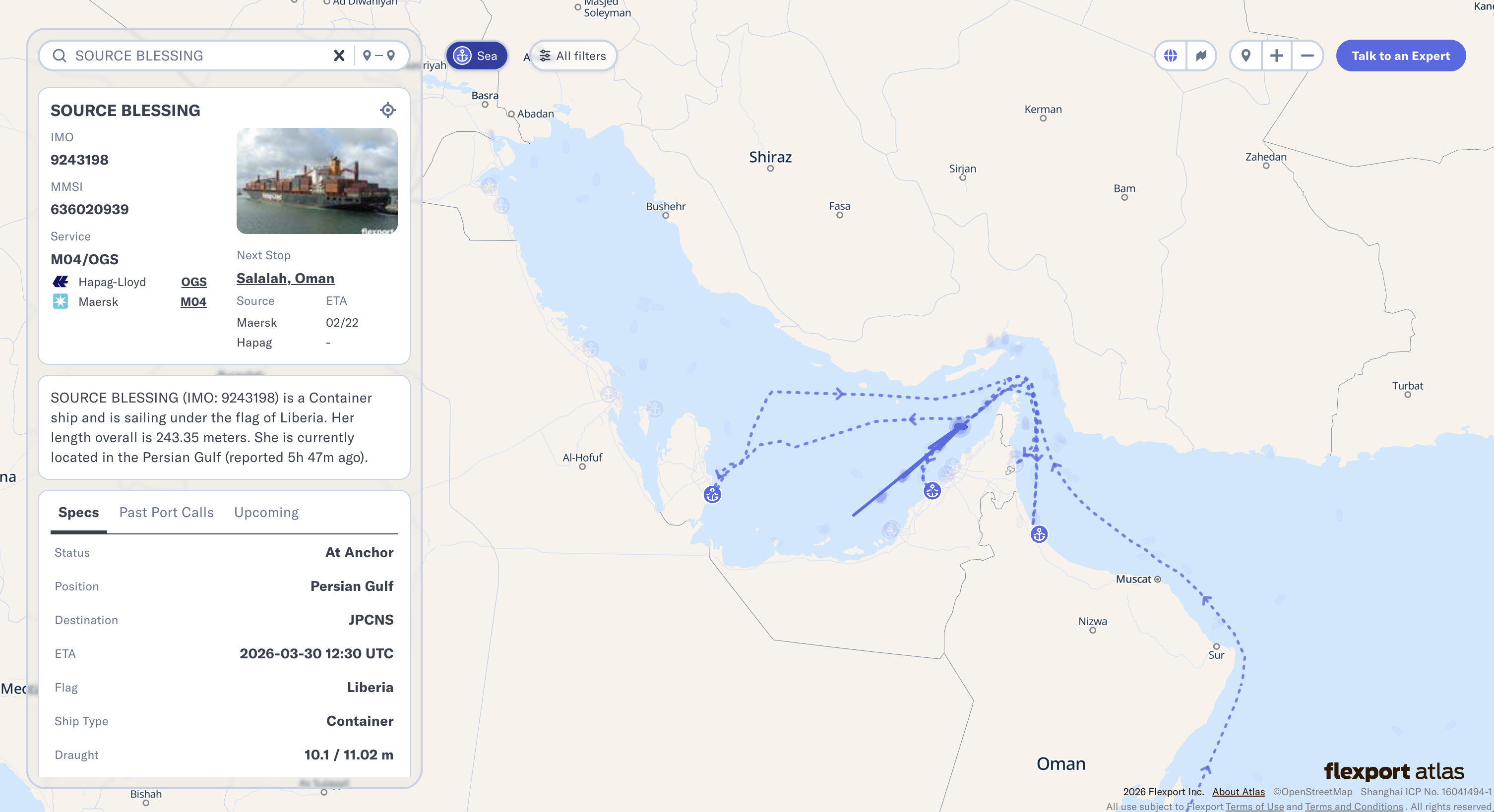

- The Source Blessing, a 3,200-TEU Liberian-flagged vessel, was struck by debris today near the port of Jebel Ali. The crew is safe, and the fire has been extinguished.

MARCH 12, 2026

Middle East Escalation Disrupts Global Ocean and Air Freight

Update: March 12, 2026

Ocean:

- The Port of Salalah has suspended operations until further notice, following a drone attack yesterday that hit several of the port’s fuel storage tanks.

- The Source Blessing, a 3,200-TEU Liberian-flagged vessel, was struck by debris today near the port of Jebel Ali. The crew is safe, and the fire has been extinguished.

- View more on Flexport Atlas.

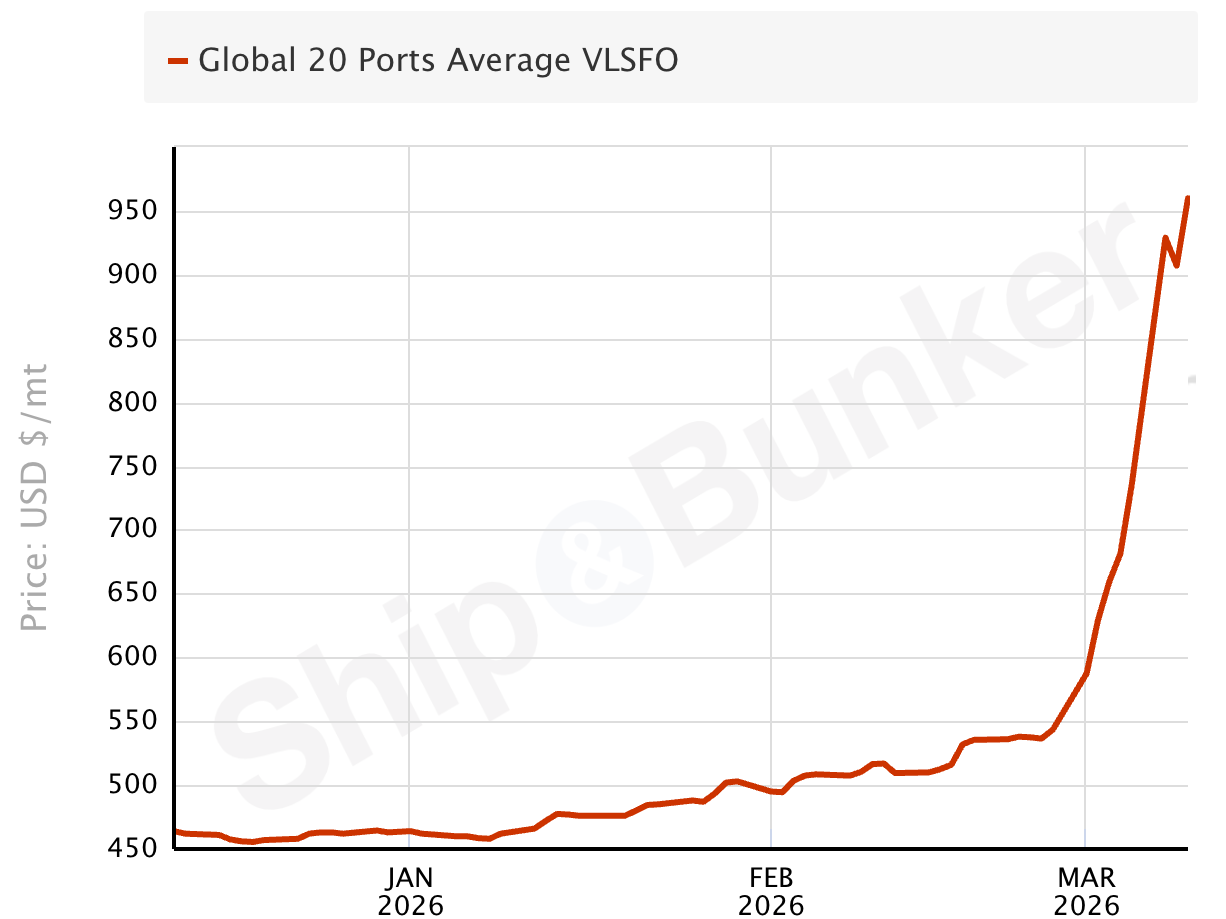

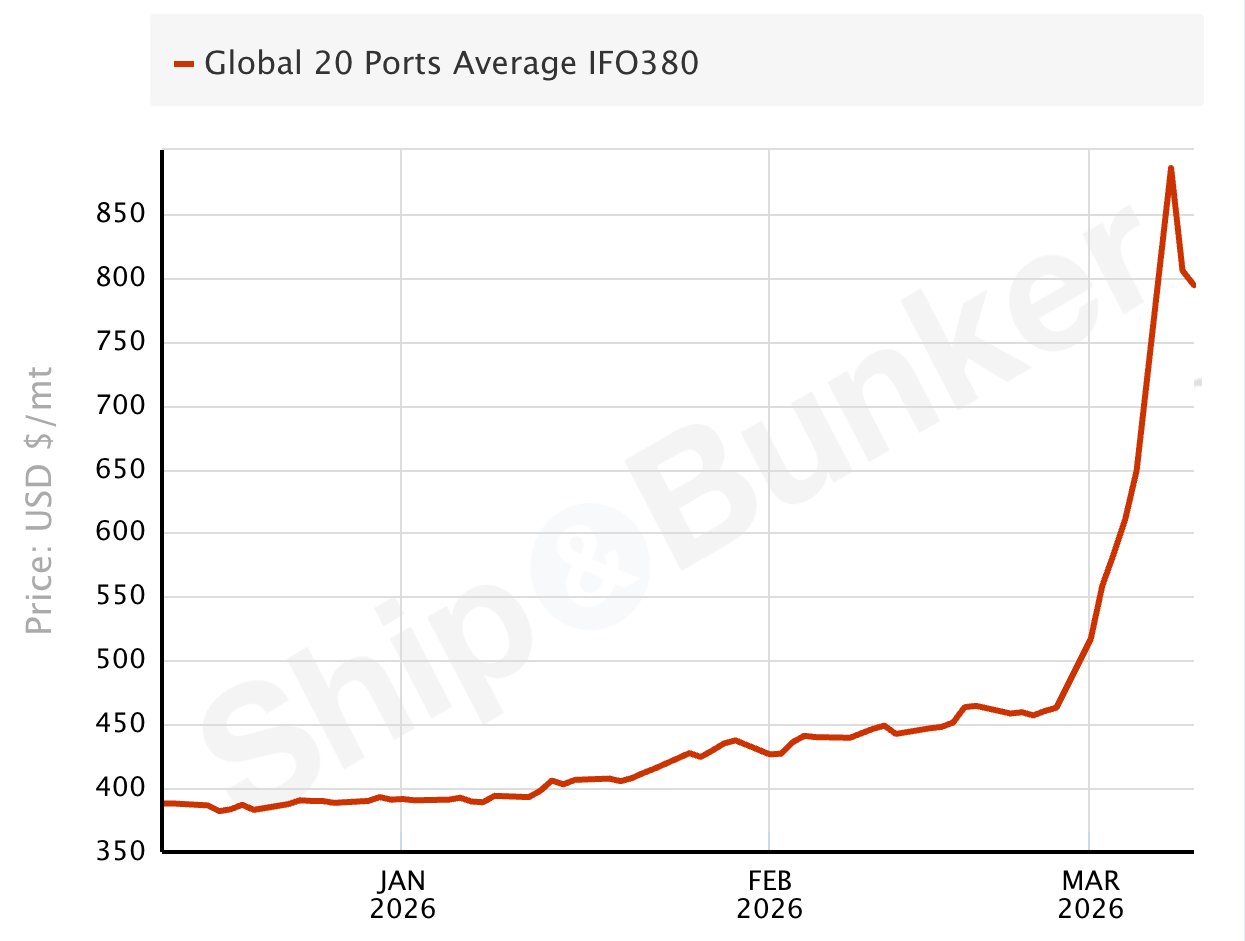

- Across the top 20 global ports, the average price of very low sulphur fuel oil (VLSFO)—used by most container ships running on fuel without scrubbers—has now risen more than 80% since the effective closure of the Strait of Hormuz. The average price of IFO380 fuel, which can be used on vessels with scrubbers, has risen more than 70%.

- Source: Ship & Bunker

- Source: Ship & Bunker

Update: March 11, 2026

Ocean:

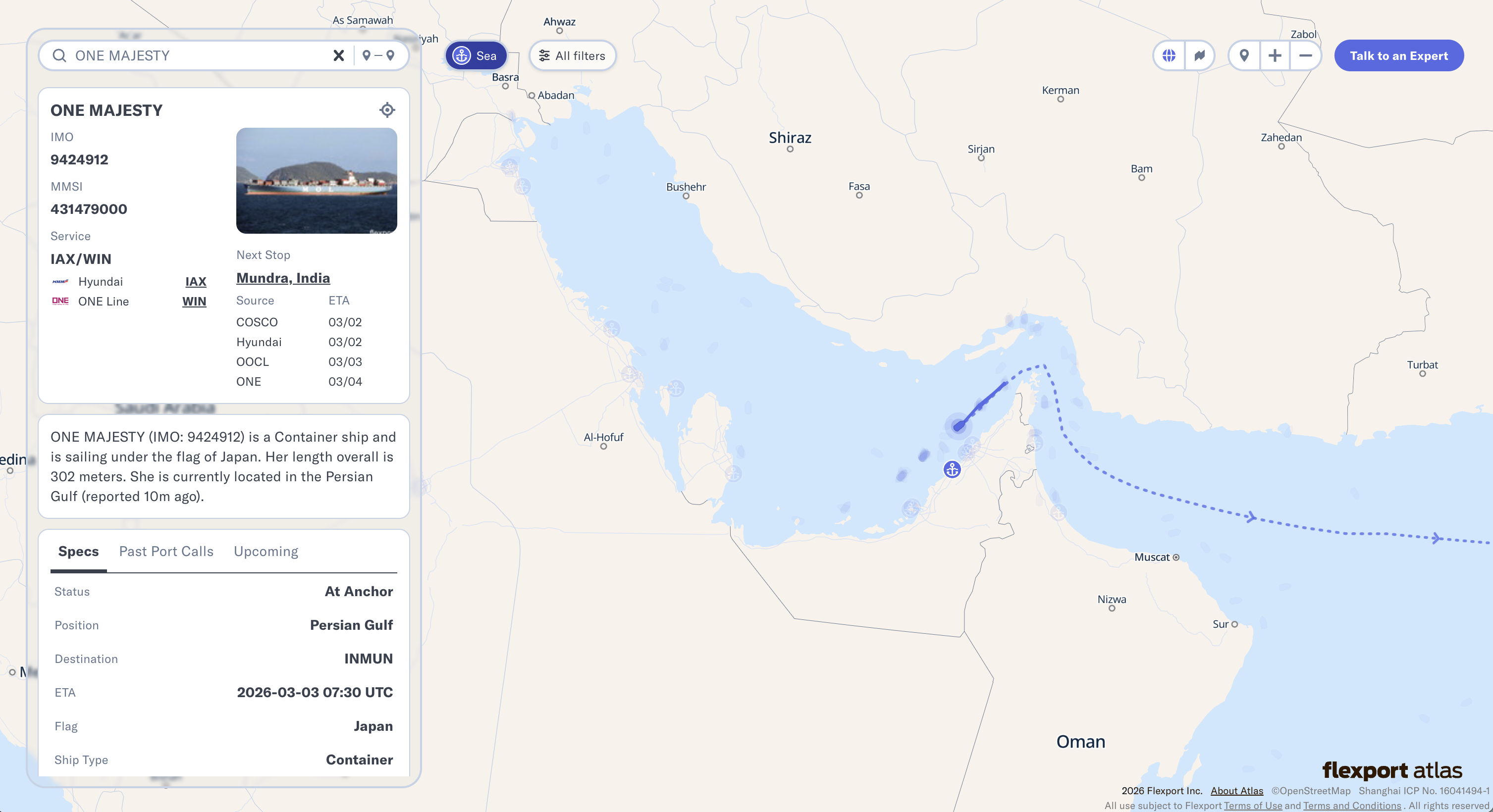

- ONE Majesty, a 6,700-TEU container ship, was impacted while at anchor today in the Persian Gulf.

- ONE has indicated that all crew members have been accounted for, and the vessel has sustained minor damage and will remain fully operational.

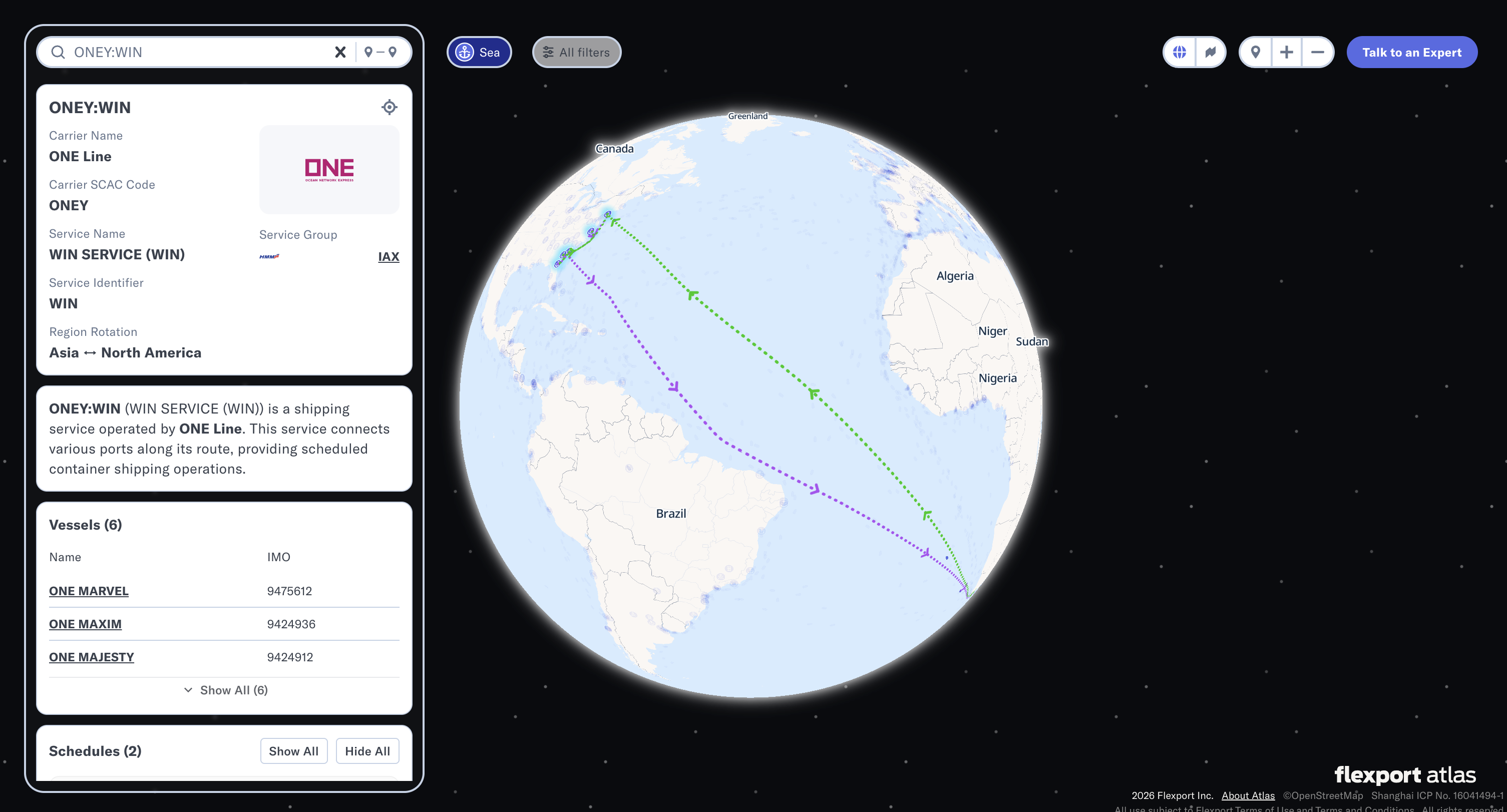

- The vessel operates on ONE’s WIN service, which connects India, Pakistan, and Jebel Ali to the U.S. East Coast.

- Monitor ONE Majesty's and other container ships' movements in real time with Flexport Atlas.

- Two other vessels were hit today, both seemingly bulk carriers or oil tankers.

Update: March 10, 2026

Ocean:

- Oil prices are increasing and remain extremely volatile.

- Brent oil hit $100 per barrel for the first time since summer of 2022, underwent a major correction, and remains elevated. Ship bunker fuel prices continue to rise, with Singapore very low sulphur fuel oil (VLSFO) doubling in the span of a week.

- Bunker markets remain regionally fragmented, with Asian fueling hubs commanding a consistent price premium over Western ports. To mitigate these operating costs, top carriers continue to leverage their scrubber-equipped vessels, which represent roughly 45% of their fleets, to capture an estimated 10-15% savings by burning cheaper IFO380 fuel instead of VLSFO.

- Carriers are implementing emergency bunker fuel surcharges on trades that do not directly touch the Middle East, effective at the end of March or the beginning of April.

- Among the top 20 fueling ports, the average price of VLSFO has already risen by 35% in the last two weeks.

- Carriers are also implementing General Rate Increases (GRIs) on Freight All Kinds (FAK) contracts for major West–East trade lanes.

- The Shanghai Containerized Freight Index (SCFI)’s Comprehensive Index increased 12% week over week, even though we normally observe decreases during this period of the year.

- At the onset of the disruption, Alphaliner estimated nearly 470,000 TEUs of total capacity were trapped in the Persian Gulf. While carriers have aggressively diverted vessels and discharged cargo at alternative safe ports where possible, Sea-Intelligence estimates that up to 200,000 TEUs of critical global deep sea capacity remain potentially trapped by the ongoing closure of the Strait of Hormuz.

- On March 6, the Mussafah-2 tugboat was struck in the Strait of Hormuz, with eight crew members feared dead. The Mussafah-2 was hit while attempting to assist the Safeen Prestige, a 1,700-TEU container ship struck in the Strait of Hormuz two days prior.

Air:

- Operational impacts: Multiple drone and missile launches have impacted the few airports in operation. Muscat remains the main hub for flight activity, while Dubai has infrequently allowed waves of flights to depart and arrive.

- Some flights began departing Qatar today, while the air spaces of Iran, Iraq, and the UAE remain closed. Saudi Arabia has partially closed its air space until March 13, specifically in the area bordering Iraq and the Persian Gulf.

- Air space closures are forcing longer flight routings, increasing fuel consumption. For this reason, airlines are reducing payloads (carrying less cargo) to accommodate the extra fuel required for extended flight routes.

- We are seeing a massive shift in capacity as forwarders and airlines scramble to find alternative routings and stable gateways.

- After prolonging its air space closure throughout the southern sector of the Baku flight information region (FIR) in response to drone strikes, Azerbaijan reopened its Iran border for cargo flights yesterday.

- Massive flight cancellations out of South Asia have delayed deliveries for many major clothing retailers. Manufacturers in Bangladesh and India are reporting shipments being left behind at airports as airlines adjust routes.

- Rate surges and surcharges:

- Market rates are climbing rapidly across key trade lanes: Europe–Middle East (+22%), Asia–North America (+12%), and Europe–Asia (+9%).

- Due to shifting conditions, airlines are frequently moving to ad hoc pricing, with some quotes valid for only 24 hours. South Korea saw a steady rate increase since last week, but the delta is only around $0.20-0.30/kg.

- Cambodia, India, Bangladesh, Sri Lanka, and Pakistan are heavily impacted by the ongoing Middle East conflict on both FEWB and TPEB trade lanes. General cargo rates for these countries have increased more than $1/kg since last Friday.

- Fuel surcharges are undergoing frequent adjustments to account for longer flight paths. Additionally, many carriers are now introducing War Risk Surcharges.

Update: March 6, 2026

Air:

- Airline status:

- Emirates: Operations resume on a "limited" basis for both passenger and freighter services. Currently, the primary focus is on clearing existing cargo backlogs; future uplift is heavily contingent on local fuel availability.

- Etihad Airways: Starting today (March 6), Etihad will resume a limited commercial schedule from Abu Dhabi. While this provides a much-needed boost to bellyhold capacity, demand is expected to far outstrip supply.

- EVA Air and Turkish Airlines: Standard bookings have been suspended in Southeast Asian hubs like Malaysia and Singapore. Currently, EVA Air and Turkish Airlines are only accepting express service at significantly elevated premium rates.

- Virgin Atlantic: The carrier is operating a limited schedule between the U.K. and UAE, with priority given to time-sensitive and critical cargo.

- Far East Westbound (FEWB) outlook: We are seeing an ongoing tightening of the air market. In addition to geopolitical rerouting, the market faces the combined pressure of a month-end "ecommerce surge" and the end-of-quarter financial peak.

- South China and Southeast Asia: Demand across South China (including Hong Kong), Vietnam, Thailand, Malaysia, and Indonesia is projected to climb sharply toward the end of March. Many airlines in these regions have already implemented "stop booking" practices to manage overflow.

- North China: While North China has seen a slight recovery in capacity as Middle Eastern carriers (Emirates, Etihad) gradually resume operations, procurement costs continue to trend upward. Market analysts expect heavy ecommerce volumes in the coming weeks, which will likely keep rates on a steady incline.

- Pricing: The market is under extreme pressure. We are tracking a dramatic increase in rate levels, specifically for shipments originating in Malaysia, Singapore, the Philippines, and India.

- Rates are increasing from all origins on the FEWB route. Notably, rates from Europe to the UAE have now escalated beyond standard express levels.

Update: March 5, 2026

Ocean:

- A tanker was hit approximately 30 nautical miles southeast of Mubarak Al-Kabeer, Kuwait, according to the UKMTO. Ballast water was observed leaking from the tanker.

Air:

- Dnata is starting to accept general cargo in Dubai for exports. We will be able to book our shipments out of Dubai. Our sea-air shipments that already arrived in Jebel Ali this week, as well as other shipments in transit in Dubai, can be shipped to EU destinations.

- Dnata has indicated that dangerous goods, live animals, perishables, and all other special cargo shipments remain excluded at this time.

- Extensive air space closures throughout the Gulf have removed 39% of international air cargo capacity (vs. pre-Lunar New Year) across the Asia-Pacific–Middle East and South Asia–Europe corridors, according to Aevean data.

Update: March 4, 2026

Ocean:

- The Safeen Prestige—a 1,700-TEU, Maltese-flagged ship owned by the Abu Dhabi Ports Group—was struck in the Strait of Hormuz today. It is the first container ship struck in the Strait of Hormuz since the start of the conflict.

- A large number of container ships are likely still trapped in the Persian Gulf and seeking shelter.

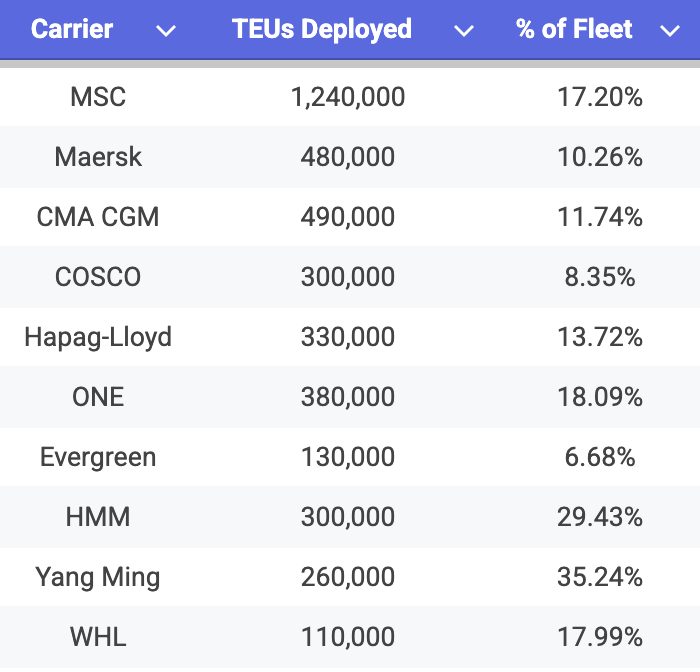

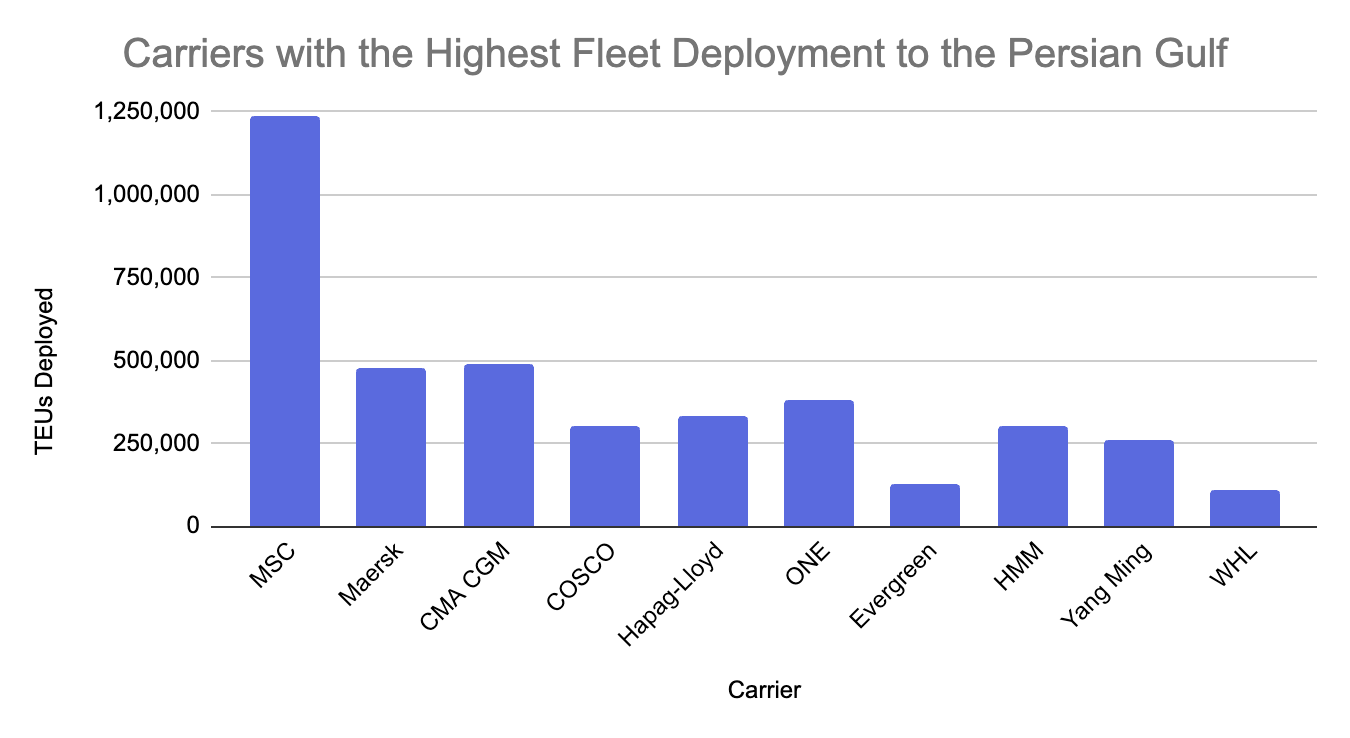

- On March 2, 2026, Alphaliner reported that 138 container ships were trapped in the Persian Gulf, accounting for nearly 470,000 TEUs of capacity. MSC and CMA CGM represent about 109,000 TEUs and 70,000 TEUs of that capacity, respectively. Other carriers with vessels in the Persian Gulf (as of March 2) include Maersk, COSCO, Hapag-Lloyd, ONE, Evergreen, HMM, and Yang Ming.

- In general, the current Middle East conflict directly impacts 10.7% of the global container fleet by TEU capacity, according to Alphaliner data. A total of 124 container liner services encompassing 520 vessels call at least one port in the Persian Gulf across pro forma rotations.

- MSC leads the top 10 ocean carriers in terms of TEUs deployed to the Persian Gulf. Meanwhile, Yang Ming leads the top 10 in terms of the percentage of its vessel fleet calling in the Persian Gulf.

Fleet Deployment to the Persian Gulf

Source: Alphaliner

Source: Alphaliner

Air: Air cargo capacity remains severely impacted due to the closure of most Gulf Cooperation Council (GCC) air spaces.

- All scheduled Emirates flights to and from Dubai remain suspended until 11:59 p.m. GST on March 7 due to air space closures across the region.

- Some non-Middle-Eastern carriers are operating cargo flights to and from Dubai. They assume no liability.

- Rates remain at COVID-high levels. Transit times are not guaranteed, with operations subject to air space availability. Sensitive cargo is being prioritized.

- Other major carriers, including Etihad, Qatar Airways, and Saudia, have suspended or re-routed services via Jeddah (JED) and Riyadh (RUH).

- Cargo operations are limited. However, cargo is slowly moving and the backlog is getting cleared.

- Network and transit impacts:

- Expected shipment backlogs upon reopening of the air space

- Congestion at origin and alternative hubs

- Transit extensions of 5 to 10+ days

- Capacity prioritization for essential cargo

- Air freight cost outlook upon the resumption of services:

- Sharp freight rate increases due to capacity shortages

- Fuel and re-routing surcharges

- Elevated ground handling and storage charges

- Potential War Risk Surcharges

- Alternative air gateways under evaluation include Muscat (MCT), Riyadh (RUH), and Jeddah (JED).

- The movement of cargo from UAE and Doha airports to alternative gateways is subject to operational feasibility and regulatory approval. Transporting goods from the UAE to neighboring countries requires full customs clearance, meaning shippers and consignees must provide additional documentation. The process may take several days to conclude.

- UAE infrastructure remains functional. The primary constraints are carrier risk decisions, routing adjustments, air space closures, and insurance cost escalations. Additional schedule volatility and pricing fluctuations should be expected until de-escalation.

Update: March 3, 2026

Ocean:

- The Port of Salalah, the biggest port in Oman and a critical gateway connection in the region for Gemini, has closed in response to a drone strike. This closure will primarily impact Pakistani cargo en route to the U.S.:

- Maersk and Hapag-Lloyd are the most impacted and exposed.

- All carriers continue to transship Pakistani cargo instead of calling directly due to complications from the Pakistan-India conflict in May of 2025.

- Hapag-Lloyd has been connecting Pakistani cargo onto TPI, its service from the Indian subcontinent to the U.S. East Coast, at the Port of Salalah.

- MSC, ONE, and CMA CGM have been loading Pakistani cargo onto mother vessels at the Port of Colombo.

- MSC has declared an "End of Voyage” for shipments to the Arabian Gulf (Persian Gulf).

- MSC is diverting cargo to the nearest safe port, where customers must arrange for their own local recovery.

Ocean impacts remain fluid, with high uncertainty. That said, we anticipate:

- Congestion at transshipment hubs and reduced schedule reliability for all Asia trades

- If the situation remains status quo for an extended period, carriers may unload containers with a final destination in the Persian Gulf at transshipment ports across Southeast Asia and the Indian subcontinent, so that their respective ships may continue their routes where able or get re-routed to service other lanes.

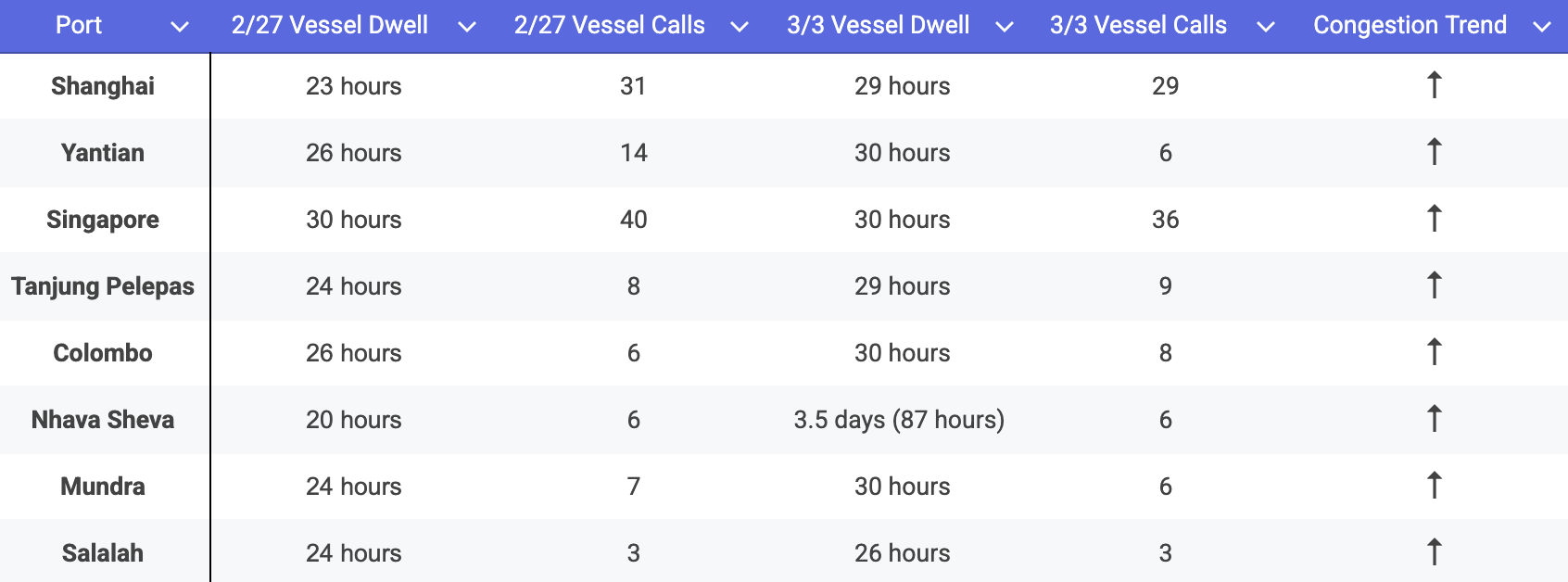

- Given that vessels are being re-routed due to the closure of the Strait of Hormuz, we anticipate growing port congestion at hubs near the Persian Gulf and in Southeast Asia (Singapore, Tanjung Pelepas, Colombo, Nhava Sheva, Mundra, and Salalah). We are already seeing a trend in berth and dwell times across many key transshipment hubs.

- Since bookings to specific destinations have been put on hold due to network disruptions related to ships taking shelter, we expect backlogs at origins and equipment issues to rise in the coming weeks.

- Cost changes: surcharges / Bunker Adjustment Factor (BAF)

- MSC will apply a mandatory $800/container surcharge to all shipments to the Persian Gulf. Customers are responsible for all additional discharge, handling, and storage expenses.

- Maersk has implemented emergency freight increases for shipments to and from the UAE, Qatar, Saudi Arabia (Dammam and Jubail), Bahrain, Kuwait, Iraq, and Oman (Sohar).

- Cargo to and from the Middle East (Red Sea and Persian Gulf) may be subject to emergency recovery charges. CMA CGM, Maersk, and Hapag-Lloyd have already announced emergency recovery charges.

- Carriers have yet to confirm if they will apply any added costs to major Arabian Sea ports of loading (POLs) like Nhava Sheva, Mundra, and Karachi.

- If the price of oil or low-sulphur fuel spikes due to constraints in the Strait of Hormuz, carriers will work to pass those increases on to shippers through emergency bunker mechanisms. We have already seen some carriers announce large rate increases that will take effect on March 15. It currently remains unclear what will be covered in normal Freight All Kinds (FAK) increases, and what will be covered under emergency surcharges.

Air:

- Partial air space closure in Pakistan: The Pakistan Airports Authority has announced a partial closure of its commercial air space until the end of March due to regional disruptions caused by the Middle East conflict.

- Daily time restrictions: Specific route segments in the Karachi and Lahore flight information regions will be unavailable daily from 9:00 a.m. to 3:00 p.m. (4:00 to 10:00 GMT).

- Duration: These daily restrictions are effective immediately (starting today, March 3) and will remain in place until March 31.

- Flight cancellations: Over 150 international flights between Pakistan and Middle Eastern destinations have already been canceled as a result of the situation.

- Lufthansa Group airlines will suspend flights to and from Dubai and Abu Dhabi until March 6. Additionally, the air space of the UAE will not be used until March 6.

- Lufthansa Group airlines will initially suspend all flights to and from Larnaca (Cyprus) through March 6, and will not be using the country’s air space.

- Riyadh is back on the regular flight schedule as of today, March 3, without transport restrictions.

- Bookings for shipments to Tel Aviv, Beirut, Amman, Erbil, Dammam, Abu Dhabi, and Dubai (DXB and DWC) are temporarily suspended until March 12 at 11:59 p.m. (local time).

- Dubai (DXB and DWC) and Doha (DOH) may resume cargo operations this weekend, assuming the conflict does not escalate further.

- Cargolux has canceled all flights to Dubai until the end of March.

- Many passenger flights, mainly operated by Emirates, departed today from Dubai International Airport (DXB). The cargo embargo still stands.

- Qatar Airways is working on an operational readiness plan to restart operations this week or early next week at the latest, assuming the conflict does not escalate further.

- Egypt has not reported anything unusual.

- We have not seen any news regarding fuel surcharge increases.

Update: March 2, 2026

Ocean: Transits through the Strait of Hormuz and the Bab al-Mandab Strait remain suspended by major ocean carriers until further notice. Other updates:

- ZIM’s headquarters in Haifa remain fully functional.

- CMA CGM and Hapag-Lloyd have both announced an emergency conflict surcharge of $3,000/FEU for cargo to and from Persian Gulf and Red Sea ports, excluding the Arabian Sea (Pakistan and India).

- COSCO has also suspended transits through the Strait of Hormuz on safety grounds, despite speculation that China-linked vessels might be exempt.

- The Israeli Ports of Haifa and Ashdod continue to operate as normal.

- Multiple tankers in the Strait of Hormuz have reportedly been stuck. These include the dark fleet vessel Skylight, the Hercules Star, the MKD VYOM, and the Ocean Electra.

- The Stena Imperative, a U.S.-flagged tanker, was impacted by two projectiles this morning in a Bahraini shipyard.

- One dockworker was killed, the American crew was evacuated from the ship, and the fire on board has been extinguished.

- War risk insurance is being withdrawn or sharply repriced.

Air: Meanwhile, air cargo capacity is shifting from airports affected by the conflict to nearby airports like Cairo and Istanbul. Airlines are sending information as they finalize decisions.

- We have been informed by Emirates staff that they will partially resume passenger operations to a handful of unspecified destinations tonight. The cargo embargo will continue until further notice.

- Lufthansa Cargo, in conjunction with the Lufthansa Group, has indicated the following:

- The air space of the UAE will not be used until March 4.

- Flights to Tel Aviv, Beirut, Amman, Erbil, Dammam, and Tehran will be suspended until March 8.

- The following air spaces will not be used until March 8: Israel, Lebanon, Jordan, Iraq, Qatar, Kuwait, Bahrain, Dammam, and Iran.

- Lufthansa Group airlines will suspend flights to and from Dubai and Abu Dhabi until March 4.

- An embargo, in effect through March 8, applies to exports, imports, and transit destined for Dubai, Abu Dhabi, or Riyadh. The embargo also applies to any shipments containing dry ice, perishable goods, valuable cargo, temperature-sensitive goods, live animals, hatching eggs, day-old chicks, or human remains.

- Etihad Airways’ commercial flights to and from Abu Dhabi will remain suspended until March 4 at 2:00 p.m. GST.

Originally Published February 28, 2026:

On February 28, 2026, a sharp military escalation in the Middle East triggered immediate closures of the Strait of Hormuz, a full suspension of Suez Canal transits, and widespread airspace shutdowns across key Gulf states. What began as a regional security crisis has now become a direct disruption to global supply chains.

Ocean carriers have diverted vessels planned for Suez transit around Africa, the Strait of Hormuz has been closed and vessels that cannot be rerouted have been asked to take shelter. Airlines have grounded flights and rerouted aircraft across longer corridors. Several providers have formally invoked force majeure, suspending standard service level agreements and transit time guarantees due to circumstances beyond their control.

Here is what we know and how Flexport is responding. To monitor the situation, you can view live container ship movements with Flexport Atlas.

Ocean Freight: Suez Canal and Strait of Hormuz Closures

The closure of the Strait of Hormuz and the suspension of Suez Canal transits remove the option for transiting Suez used by some Ocean carriers for Indian Subcontinent to Europe and US East Coast, while simultaneously blocking access to key Gulf hubs.

What makes this disruption particularly significant is that some Asia–Europe services had only recently returned to Suez.

On the Asia–North Europe trade, CMA CGM had officially resumed Suez transits for its flagship FAL 1 and FAL 3 services, connecting Shanghai, Ningbo, and Yantian with Southampton, Hamburg, and Rotterdam. The return to Suez reduced full-loop transit times by seven days, from 105 days down to 98 days. That efficiency gain has now been reversed, with both services pulled back to Cape routing.

Within the Gemini Cooperation, Maersk and Hapag-Lloyd had previously announced that AE12 and AE15 services were next in line for a structural return to Suez, following initial adjustments on ISC-focused services. Those plans have now been formally rescinded.

On the Asia–Mediterranean trade, CMA CGM’s MEX service, linking Asia with Valencia and Fos-sur-Mer, had briefly returned to the Suez route earlier this year. It has now reverted to the Cape. Similarly, Gemini’s SE1 and SE3 services were being upgraded to 20,000 TEU vessels with the intent to route via Suez and improve reliability in the Adriatic and Spanish regions. Those structural changes remain in place, but the Suez routing component has been withdrawn.

For Transpacific services between Asia and the U.S. East Coast, the impact is more limited. Most services were already avoiding Suez, with the exception of certain Indian-Subcontinent-linked routings. The broader Transpacific network remains largely unchanged from a routing perspective, though equipment imbalances and capacity tightening may create secondary effects.

Across alliances, the response has been consistent. Vessels scheduled for Suez are being rerouted around Africa. Far East–Red Sea services are suspended. Cargo destined for Gulf ports is being held at transshipment hubs or diverted to alternative Mediterranean and African gateways. Some carriers have also suspended new bookings to Persian Gulf destinations until safe feeder or land-bridge solutions can be confirmed.

For shipments currently inside the Persian Gulf, the situation is more immediate. Vessels have been instructed to take shelter at major hubs such as Jebel Ali, Abu Dhabi, and Doha. Cargo on those vessels is effectively paused until safe passage can be reestablished.

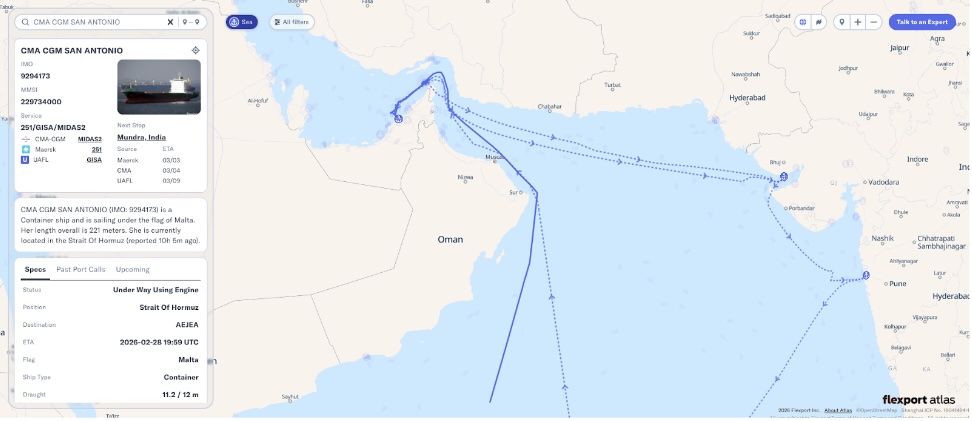

Example: CMA CGM SAN ANTONIO left Jebel Ali on February 28, and is now unlikely to arrive to Mundra, India by Monday, March 2.

The operational consequences are significant.

Transit times between Asia and Europe, and on certain Asia–U.S. East Coast lanes, are expected to increase by 10 to 14 days as vessels detour around the Cape of Good Hope. That extension places additional pressure on equipment availability, schedule reliability, and network capacity.

At the same time, we anticipate:

- Emergency diversion fees and war risk surcharges

- Spot rate increases driven by capacity tightening

- Port congestion at alternative Mediterranean and Southeast Asian gateways

As carriers discharge Gulf-bound cargo elsewhere and rebalance networks, secondary bottlenecks are likely to emerge.

Air Freight: Widespread Airspace Closures

The disruption is not limited to ocean freight.

On the same day, coordinated military strikes between the United States, Israel, and Iran led to the immediate closures of sovereign airspace across Qatar, the UAE, Saudi Arabia, and Kuwait and immediate suspension of operations to and via the Middle East for most airlines.

The closures of Middle East hubs (Doha, Dubai, Riyad, Bahrain) reduces global capacity and specifically impacts Asia - Europe, Asia - Middle East and Europe - Asia Air Trade.

Several carriers have suspended regional operations to, from and via the Middle East and invoked force majeure. Middle East carriers which represent 13.6% of global capacity (source: IATA) in particular are unable to operate the majority of their flights. Their operations will be disrupted beyond the trade between Asia - Middle East - Europe.

With airspace inaccessible and safety risks elevated, most shipments originating in, destined for, or transiting through the Middle East are being grounded or diverted. Service levels and transit guarantees are currently suspended by the airlines.

The Middle East carriers stoppage, combined with the longer and more fuel-intensive rerouting required by European and Asian airlines, is reducing effective global capacity and increasing costs to operate. We expect immediate volatility, including a sharp increase in airfreight spot rates, suspension of longer term rate agreements under force majeure and growing backlogs on key Far East corridors.

Even lanes not directly tied to the Middle East will feel secondary pressure as aircraft and crews are redeployed across longer routes.

How Flexport Is Responding

Our teams are actively responding to protect our customers’ cargo and minimize disruption.

For ocean freight, we are evaluating alternative routings and, where appropriate, Sea-Air solutions through Southeast Asia to bypass affected zones. For air freight, we are in active negotiations with non-Middle Eastern carriers to secure remaining capacity and identify alternative routings and gateways for shipments on Asia - Middle East - Europe trade.

All diversions, vessel shelter positions, and flight adjustments are reflected in real time on the Flexport platform. Customers can monitor shipment status directly through Flexport Atlas, as well as in the Flexport Platform, while dedicated account teams are proactively reaching out to those with cargo currently sheltered, grounded, or diverted.

In parallel, we are working closely with carrier and airline partners to model recovery scenarios and longer-term schedule adjustments. As clarity emerges, we will provide structured guidance on stabilization timelines and contingency planning.

What to Expect

In the near term, businesses should prepare for longer lead times, tight capacity, elevated rates, and continued volatility across both ocean and air networks.

This remains a fluid situation. Operational directives are evolving quickly, and conditions on the ground and in the air may shift with little notice. We are committed to providing transparent, timely updates as new guidance is issued.